Recognizing the Basics of Securing a Home Loan Funding for Your New Home

Starting the journey to protect a mortgage for your brand-new home requires a detailed grip of numerous basic aspects. The selection of home mortgage types, subtleties of rate of interest, and the critical duty of credit report all add to the intricacy of this process. As you browse the myriad of options and demands, comprehending exactly how these elements interplay can be crucial to your success. Yet, what really equips potential homeowners is usually forgotten. Could there be an essential technique that simplifies this apparently difficult undertaking? Let's check out exactly how to effectively approach this vital economic choice.

Sorts Of Mortgage

Browsing the varied landscape of home loan is critical for possible home owners to make informed monetary decisions - mortgage loan officer california. Recognizing the different kinds of home loan lendings available can significantly influence one's option, lining up with economic goals and personal conditions. One of the most typical types include fixed-rate, adjustable-rate, FHA, VA, and big finances, each serving distinct needs

For people with limited deposit capacities, Federal Real estate Administration (FHA) financings give a feasible option, calling for lower deposits and credit rating. Veterans and active-duty army members could receive VA car loans, which offer affordable terms and frequently call for no deposit. Big car loans provide to buyers in high-cost locations seeking to fund properties surpassing standard car loan restrictions.

Choosing the ideal home mortgage type includes reviewing one's economic stability, future plans, and convenience with threat, guaranteeing a fit pathway to homeownership.

Comprehending Interest Rates

A fixed interest rate continues to be continuous throughout the lending term, offering predictability and stability in month-to-month repayments. In contrast, a variable or adjustable-rate mortgage (ARM) might start with a reduced rate of interest price, however it can change over time based on market problems, potentially increasing your settlements considerably.

Rate of interest prices are mainly affected by economic aspects, including rising cost of living, the Federal Book's financial policy, and market competition amongst loan providers. Borrowers' credit history and financial accounts likewise play an essential role; greater credit rating scores usually protect lower rates of interest, showing minimized risk to loan providers. Therefore, boosting your credit report prior to making an application for a mortgage can lead to substantial cost savings.

It's critical to contrast deals from multiple loan providers to ensure you secure one that site of the most beneficial price. Each percent factor can influence the long-term price of your home loan, emphasizing the relevance of comprehensive research study and informed decision-making.

Funding Terms Discussed

A secret element in understanding mortgage agreements is the funding term, which determines the period over which the customer will repay the lending. Usually revealed in years, funding terms can dramatically affect both regular monthly settlements and the overall rate of interest paid over the life of the funding. The most usual home loan terms are 15-year and 30-year durations, each with distinctive advantages and considerations.

A 30-year financing term enables for reduced regular monthly repayments, making it an attractive alternative for lots of property buyers seeking affordability. This prolonged repayment duration typically results in greater overall passion costs. Alternatively, a 15-year financing term typically includes higher regular monthly repayments however offers the benefit of reduced passion accrual, making it possible for property owners to construct equity faster.

It is essential for consumers to assess their monetary circumstance, long-term goals, and threat tolerance when choosing a lending term. Furthermore, recognizing other variables such as prepayment charges and the capacity for refinancing can offer additional adaptability within the chosen term. By very carefully considering these elements, debtors can make enlightened choices that align with their financial goals and make sure a manageable and successful home loan experience.

Value of Credit Rating

Having an excellent credit history can substantially affect the terms of a home mortgage financing. Consumers with greater ratings are usually offered reduced rates of interest, which can lead to significant cost savings over the life of the funding. Additionally, a solid credit history may raise the probability of car loan authorization and can offer better negotiating power you can try this out when going over funding terms with lenders.

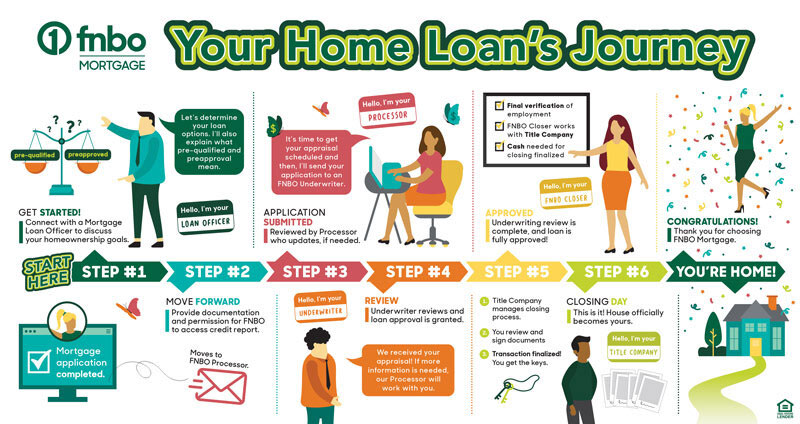

Navigating the Application Process

While debt scores play a pivotal role in protecting a home loan, the application procedure itself requires cautious navigation to make certain a successful outcome. The process begins with collecting essential paperwork, such as proof of earnings, income tax return, financial institution declarations, and recognition. This documentation provides lenders with an extensive view of your monetary security and capability to pay off the loan.

Next, research study various lending institutions to contrast rate of interest prices, car loan terms, and fees (mortgage loan officer california). This action is crucial, as it aids determine the most beneficial home mortgage terms customized to your economic see here now scenario.

During the mortgage application, make certain accuracy and efficiency in every detail provided. Errors can bring about delays or even rejection of the application. Additionally, be gotten ready for the lending institution to request further details or information throughout the underwriting procedure.

Verdict

Protecting a home mortgage financing calls for a thorough understanding of numerous elements, including the types of loans, rate of interest, financing terms, and the duty of credit rating. Fixed-rate and variable-rate mortgages each have special benefits and risks. A solid credit history can considerably affect the terms offered by loan providers. Thorough preparation with essential documentation and positive contrast of lending institutions can improve the likelihood of acquiring positive terms. Reliable navigation of these elements is necessary for an effective mortgage application process.